How To Buy A Small Multifamily Property: A Step By Step Case Study

I really like small multifamily properties, and I talk about them an awful lot. Several months ago, I wrote a post called “How to Make a Million Dollars in Real Estate” which was designed to show the possibilities for building wealth through real estate – and the start of that plan was the purchase of a small multifamily property. I’ve explained many times that the goal isn’t to buy a property that fits exactly the description mentioned, but rather to teach the math behind the method. You could buy a triplex, a few duplexes, lots of single family homes, or whatever.

It’s the cash flow that really matters.

Since that post came out, I’ve been asked by a number of people how they should buy such a property. So, to help with this, I wrote this post to show you step by step how I managed to buy my newest real estate investment, with almost nothing down and significant monthly cash flow. It’s often easy to get caught up in the “theoretical world” of how real estate investing works – so hopefully this post will give you an idea of how real estate investing can (and does) work in the real world. All the numbers in this are true and accurate, though I sometimes might round slightly for simplicity! This post is quite long, so be sure to fully understand each part before moving on, so you don’t get overwhelmed! If you have any questions at all, please leave a comment below and I’ll do my best to help answer them.

(Before I get too deep in this post, I want to invite you to download our book “The Ultimate Beginner’s Guide to Real Estate Investing” which will help you build a solid foundation for your financial future. In other words – you are going to learn exactly how to get started building wealth with real estate! To get the book, just click here and join BiggerPockets, the free real estate investing social network!)

Finally – I’d love it if you shared this on your Facebook, Twitter, G+, or whatever social network you use! So with that, let’s get to it! Let’s go back a couple months and start at the beginning (a very good place to start…)

STEP ONE: THE 5 MINUTE ANALYSIS

A lot of people struggle with math. It’s understandable because, although it isn’t terribly difficult, it can be overwhelming to get going. So, I had the idea that it would be neat to show the BiggerPockets community how I analyze an investment property in under five minutes. This isn’t the real in-depth analysis (which we’ll get to) but simply the first “filter” to decide if the property is worth pursuing.

I sat down at my computer and pulled up Realtor.com and picked a property pretty much at random to analyze. I made a quick video (it actually ended up being slightly longer than 5 minutes, but close enough!) and I looked at some of the important aspects of this property. Specifically, I looked at:

- The location – the property is located in the town I do most of my investing in or around. I knew the location fairly well, because I own another property on the same street. I’d probably classify this as a “C+” area, maybe “B-” with mostly rentals. The property was listed at $120,000, but had originally been listed at $140,000.

- The number of units – Four units total – three 1 bedroom and one 2 bedroom.

- The rent it brings in – The listing stated a total monthly income of $1740 per month, and because I know the area well, I knew a typical one bedroom would rent for (at minimum) $400 in my area and a typical two bedroom would rent for about $500, bringing the total monthly conservative income to $1700.

- The expenses based on the 50% rule – 50% of the income left $850 to pay the mortgage.

- The cash-flow, based on the 50% rule – I looked at the total mortgage amount for a $100,000 loan (buying at $120k and putting roughly $20,000 down).

- The seller

I determined that this property was a bank repo, that had originally sold for $149,777 but the bank had foreclosed on it and was selling it at a steep discount.

The purpose of this 5 minute process is not to nail down the specifics on a property. I don’t drive out and look at it yet, I don’t make a lot of phone calls or even show my wife yet. I do this same process dozens of times every week, mostly in my head in under a minute. There are two prices to note about the properties I examine:

- The List Price: For 99% of properties I find on the MLS, the price is far too high and not worth it.

- The Ideal Price: For 99% of properties I find on the MLS – there IS a price that would make it worth it, and I like to find out what it is. That’s the point of the video above.

Some investors choose to offer the #2 price on every property they see, and while I don’t think this is necessarily a bad idea, I’d rather not waste the time on properties that I’m not a fan of. My personal strategy is to buy a few, amazing properties per year, rather than dozens or hundreds. I like the simplicity, and I’m not looking to be Donald Trump. However, when I find a property that excites me, and the listed value is somewhat in the ballpark of the ideal price, I will investigate a little closer.

Summary of the Quick Analysis

By the end of the video, I stated that “At $100,000 – this property starts getting very interesting to me.” Why? Because I like to see a MINIMUM of $100 per unit, per month on a property with nothing down using the 50% rule. If I’m putting down a large downpayment, I want to see $200 per month in income. At $100,000 with nothing down, the projected cash-flow would be right around $300, and purchasing it at $100,000 with 20% the cashflow would be around $200 per month. That would be an okay deal. However – if you know me – I don’t want an okay deal. I want a great deal. Don’t you?

Let me show you how this turned from okay to great…

STEP TWO: THE CLOSER LOOK

After publishing the video on BiggerPockets, I kinda forgot about the property. I’m not exactly sure why, but I figured I’d take a look later and just kinda dropped it. A couple weeks later I was driving near the property and remembered it, so I took a drive by. (Silly, yes, I know!) I called my real estate agent and asked him to meet me over there to look at it. Because three of the units were currently rented, we could only get in the fourth unit to check it out without giving 24 hour notice (which I don’t like to do unless I’m really really interested.) I was surprised by the overall cleanliness of the unit, though while the unit we were in was listed as the “two bedroom” unit – it was functionally only a one bedroom (one of the bedrooms was really more of a walk-in closet.) However – at this point the deal got a little better for me because I realized the units were not as ugly on the inside as they were on the outside. I could easily expect $450 per month in rent from these units, not the $400 previously thought.

THE GAME CHANGER

While looking at this property, my Agent told me something else exciting about it: this property was not a 4-plex, but actually a 5-plex. The bank had “decommissioned” the 5th unit in order to make the sale easier (4-plexes are MUCH easier to finance than 5-plexes, because a 4-unit is considered “residential” in the loan world where 5 units and up are considered “Commercial” and require a whole different set of standards and a much different approval process.) We walked to the third floor and I was shocked at what I found – a large, 3 bedroom apartment that was in decent shape. The sellers had locked all the bedroom doors and called them “storage” for the other four units.

Boom.

The numbers I had run before were based on 4 units and $1700 per month in income. Now, it seems, the potential for income was MUCH higher. This was the catalyst to turn this 4-plex from a good deal to a great deal.

A QUICK ESTIMATE OF REPAIRS NEEDED

Overall, the property was in pretty good shape, though as you can see in the photo – it looked pretty ugly from the outside (my favorite, really! It drives away competition!) It definitely needs a new paint job on the outside, and some of the shingles from a fairly new roof had blown off in a freak windstorm we had several years back (missing shingles are very common in my area because of that storm, though most homes have been fixed since then. This place had not.) Additionally, the 5th unit needed some help to bring it into a rentable shape. I estimated about $10,000 worth of work to get the place fully finished, including finishing up the 5th unit.

Immediately, I recalculated my numbers based on the new unit that I could eventually get rented out. As it turned out, it looked like this:

Units 1-4 rent: $450 each x 4 = $1800

Unit 5: $600

Total Income: $2400

x 50% expenses: $1200

Mortgage at $100,000 = $550/month ($650/month cash-flow)

Mortgage at $90,000 = $470/month ($730/month cash flow)

Mortgage at $80,000 = $430/month ($770/month cash flow)

Remember, these numbers are based on having no money down – so they are far above my threshold.

THE OFFER AND NEGOTIATION

Before I let you know the details about my offer and negotiation – understand that this strategy worked for me, in my market, because I knew my market. The market has not exploded like the rest of the country seems to have, and there is not a mass amount of competition for this kind of property here (another benefit of small multifamily properties… often less competition.) Last week, Clay Huber wrote a great article about making your first offer your “highest and best” instead of worrying about negotiating up and down, so you don’t miss out on deals. I agree, this is generally the best way to go in a busy market, but since I figured I had time and no real pressing competition- I sent a low ball offer first: $80,000.

Before I get into negotiations – I want to share one more thing that I tested on this offer. Although this was a bank REO, I also know that this was a small, local community bank with a very small department (or one person, probably) in charge of approving or rejecting offers. As such, I added a touch of “personality” to my offer – something usually only done with private sellers:

I drafted up a one-page cover letter that briefly explained that my wife and I wanted to buy the property for our portfolio, and we are local investors and we want to improve the neighborhood. Then – we included a photo of us ON the paper. My theory was that the person in charge of accepting an offer would feel more inclined to sell to a local nice couple than some faceless investor. Before doing so, I actually went on to the BiggerPockets Forums and asked if anyone had done this – and received a mostly “Well, it wouldn’t hurt” response. So I tried it – and I think it kinda worked…

The official offer I had my agent draft up on the Realtor® form basically consisted of:

- $80,000 Cash Offer

- No Financing Contingency

- 7 Day Inspection Contingency

- Close in 45 days.

- $1000 in earnest money

So I submitted the offer, via my agent, and surprisingly, the selling agent didn’t laugh at us but actually said “well, that might work.” The next day I got a call from my agent saying they verbally accepted but had to hand it upward to get signed off! I was super excited, but after several days of no response, I finally heard back that the deal was killed when the man in charge said “We will not take a $40,000 loss on this property!”

I said okay and let it go.

Several days later, the sellers called my agent and asked if I could do $100,000 and close in two weeks. I told them no (this is all verbal.) but if they sent something over in writing for $90,000 – I would accept it and close within two weeks. This kind of weird verbal negotiation went on for several days. Finally, after a week of negotiations, the bank signed off on $90,000 and they would do a few thousand worth of repairs that they had planned on doing – and I would close in two weeks. With that, I had a deal under contract. It might not be the $80,000 I really wanted, but it’s still a killer deal at $90,000.

The takeaway from this section on negotiations: every single negotiation and deal I have ever done with a bank has been unique. No two deals have ever been the same for me. It’s always a little weird.

THE INSPECTION

Because I had seven days to inspect the property, I immediately set out to arrange my inspection. After all – I had not even been inside 3 of the units because they had renters in them and I didn’t want to waste everyone’s time until I had time to get inside. This is why the “inspection contingency” in the offer was a non-debatable clause.

If you are just beginning – I highly recommend that you hire a professional home inspector to go through any property with a fine-tooth comb. On this property I hired my favorite contractor to go through the property with me, so we spent several hours running through every aspect of the property, and he gave me a bid at the same time. We crawled onto the roof, under the building, in each unit, every closet, every fridge, every nook and cranny. In the end – I saw nothing that surprised me which is always nice.

My early analysis of repairs needed were almost perfect – $10,000 to get it painted and get the 5th unit fixed up and ready to go.

A DEEPER ANALYSIS AND THE ONE-HOUR AWKWARD WEBINAR

At this point, I had looked over every square inch of the property and had an accurate look at how much this would take to fix up. I also knew generally how much everything would cost. As I discussed earlier – I had already done my quick “5 minute” analysis of the property and decided it was worth pursuing. However, a quick analysis – and the 50% rule – are only “rules of thumb.” It was time to actually dig into the numbers and make sure this property would actually pencil out the way I think it would.

Since I started this project with the BiggerPockets Community, I thought I would continue it by doing my in-depth analysis with the BiggerPockets Community as well. So, I scheduled a Webinar and gathered all my numbers ahead of time and then live, in front of dozens of BiggerPockets Members, I spent a very awkward hour explaining the deal live on the internet via the first BiggerPockets Webinar. If you missed it – you can watch a replay below (though, it’s an hour long, so be prepared!)

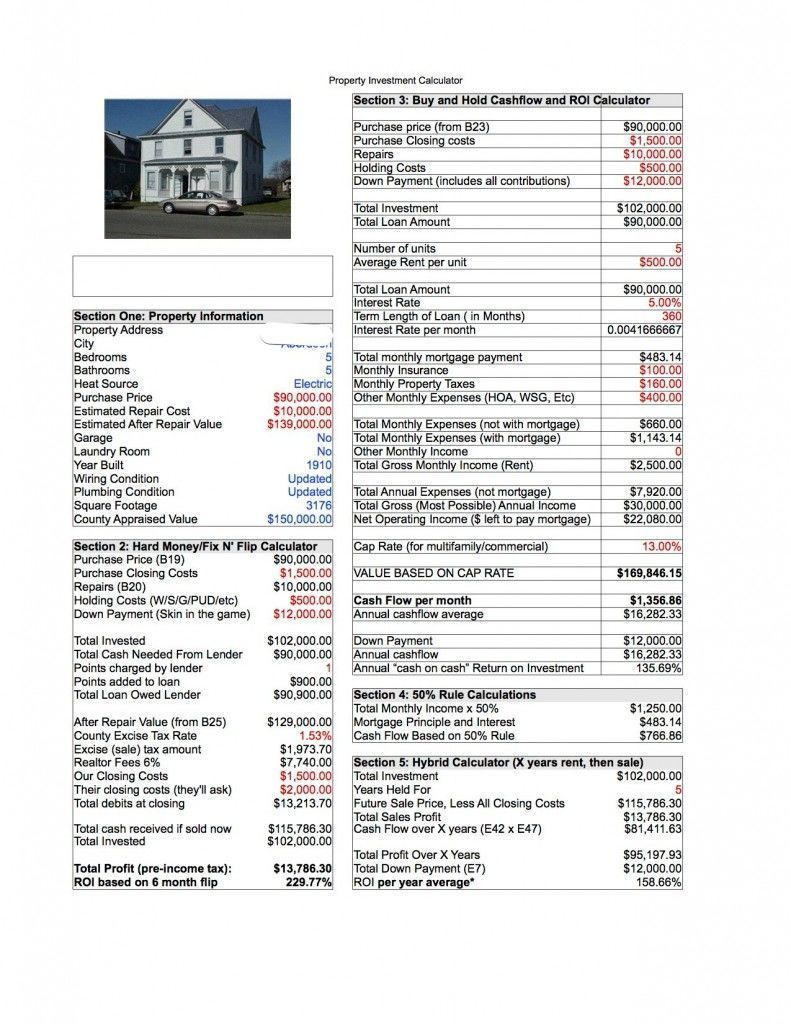

The numbers looked even better than I had hoped. I entered all the numbers into my trusty spreadsheet and came up with the following spreadsheet:

According to my spreadsheet, in a perfect month when I had no repairs and no vacancies, I would be cash flowing a $1356.86 per month! This, however, is where most newbies screw up! This is also why the 50% rule is so important. I understand that in reality, I will have repairs, I will have vacancies, and I’ll need to plan for them. I don’t have a separate spot on the chart above for vacancies and repairs (I include it under “other monthly expenses”) but I typically assume around 10% of the monthly rent for vacancies/repairs and another 10% for long-term/big-ticket planning (new roofs, new parking, etc.)

FINANCING

I delayed talking about financing until this point, but understand that I had been working the financing angle from the beginning – even before I found the property. I always make sure I have several avenues to buy a property before I offer on one – or else I’m just wasting everyone’s time.

If you’ll recall, I initially asked for 45 days to close – which would give me plenty of time to go with a conventional loan. However, when I agreed to a two-week close, I closed that option off to me. Instead, I made a call to a private lender that I had actually met through BiggerPockets (You probably know this lender – J Scott, from the BiggerPockets Forums and 123Flip.com … I actually found out on “the air” that he was a private lender, when we interviewed him on the 10th Episode of the BiggerPockets Podcast! This is why building solid relationships on BiggerPockets is so important!)

I explained the deal, sent him all the paperwork, and requested the full purchase price – $90,000. He looked it over and agreed to fund the deal. I would cover the repairs and closing costs and he would cover the purchase price. I would be taking a one-year note (meaning, I’d have to pay the whole thing off in less than one year. More on that in a second.) Thus, I would need about $12,000 in cash to make this deal happen ($10,000 in repairs, $2000 in closing costs.)

Perhaps you have heard about the “65% ARV” number that most hard money lenders stick to when making deals, and perhaps you are wondering how I got the full purchase price covered? A few thoughts on that:

- Funding the whole $90k was very generous. If you are just starting out, a private lender or hard money lender may not lend the full amount, even if you are under the 65% number. That’s just the truth. However, there are MANY lenders out there -so get to know a lot of them. Their terms may differ quite a bit. Be sure to check out the BiggerPockets Hard Money Lender Directory for the most comprehensive list of lenders available.

- The after-repair value of this 5-plex would be around $150k or more – so I am under the 65% so the lender was covered.

- I have been building my reputation for many years on BiggerPockets, which helped the lender feel comfortable lending on this project.

- The property was already rented – thus the cash-flow was there to pay the lender each month – meaning he had even less risk. With a typical flip, there is no income coming in at all, which means YOU have to pay the loan each month. Having tenants pay the bill definitely helps on this front.

But wait… a private loan is going to be short term!? What then?

Like I said, I asked for a one-year loan on this property.

Why one year?

It comes back, again, to my desire to have multiple exit strategies with everything I do. I cannot stress this point enough – you need to ALWAYS have multiple exit strategies. So, my strategies are as follows:

- Refinance the Property Through a Bank– This is my first plan, and I am 99% confident this will happen. I was already pre-approved through a bank to buy this property in the first place, so unless something drastic changes in the lending world in the coming months – I can refinance this without a lot of problems. However, in order to refinance – the bank requires that it be “seasoned” for 6 months- meaning I have to wait six months before the refinance will go through. Knowing that my monthly payment will drop significantly once I refinance, you can bet on day 6 months and one day – I will be closing on that refinance. However, if that doesn’t work, there is always option 2:

- Find a long-term private lender– If the lending environment changes and I cannot get a loan, I would look for a private lender who wanted a long-term investment. With the stability of the property, and the magnitude of the deal, I’m confident I could find a wealthy individual looking to earn a solid interest rate for 15 years or more.

- Add a Partner on and Refinance– If I couldn’t find a long-term private lender, I would bite the bullet and find a partner to add to the deal. I’ve talked about this strategy a number of times, and while I would be giving up a significant portion of equity, it would work to get me out of the deal. I have a partner who I’ve worked with on a few projects who makes great money, has excellent credit, and a stable job – so getting a loan is as easy as signing a piece of paper for him. I would simply add his name to the title on the loan, wait for the seasoning to end, and have him refinance the deal. Again, this isn’t ideal – but it’s an exit strategy (and would be excellent for him!)

- Fix and Flip– Finally, if all other options were not possible, I would simply sell the property. With the $2400 per month in income this property produces, I know I could make a hefty profit by simply selling it. However, this is my last option because I don’t care about the $30,000-40,000 I would make – I care about the $800 per month I will be making if I can get exit strategy #1 to turn out!

But what If I don’t have any money!!?

Like I said earlier, the private lender will be funding the purchase price of $90k on this deal, and I will be funding about $12,000 in repairs/closing costs. But what if I didn’t have that money? Because I’m a big fan of learning how to invest in real estate with no money, let me share just a few ideas:

- Credit Card– I could pay for all the repairs on credit. I don’t necessarily recommend doing this, but it is possible. For a good article on using credit cards to buy real estate, check out Ali Boone’s article “How to Buy Real Estate With a Credit Card.” **

- Partnership– I’ve mentioned this before – but I could add a partner to the deal. I could find a friend with an extra $12,000 and offer him part of the deal.

- Another Private Lender– Finally, I could use another private lender and borrow the $12,000 secured with a 2nd mortgage on the property. This would probably be the most difficult to do – but also plausible.

Remember – there are not a whole lot of “rules” when it comes to investing in real estate, and one of my goals of this epicly long post is to bring you inside my mind and share some of the ways I look at creative real estate investing. Before moving on, I want to share a tweet quote from one of my favorite author’s Ken McElroy, who wrote The ABC’s of Real Estate Investing (which, if you haven’t read – you need to pick up a copy right now… click here to find it on Amazon and order yourself a copy.)

You do not need a lot of money when investing in multifamily properties. What you DO need is a good deal.

— Ken McElroy (@kenmcelroy) April 1, 2013

See? Ken agrees.

THE CLOSING

In my state, we close real estate transactions with Title Companies, though in some states you might use an attorney. Either way, the process is pretty much the same.

Let’s do a quick re-cap:

- Found the property online

- Did a quick, 5 minute analysis of it

- Walked through the property quickly

- Offered on the property

- Negotiated on the property and finally agreed on terms

- Inspected the property

- Arranged financing

At this point, I was ready to proceed. My real estate agent sent over the “Purchase and Sale” agreement (the signed agreement between both parties) to the Title Company and the Title Company went to work. It took about a week or so to finish the process, where they did a title search and prepared all the documents, including the “Promissory Note” and “Deed of Trust” between myself and the private lender. I arranged for insurance (which was a little less than I thought!) and made an appointment to sign the documents.

So, last week I closed on the property. As an added bonus, the property management company who was looking after the place before closing actually found a tenant for the 4th unit before closing, so I inherited the property completely full (except for the 5th unit.)

Going forward – I will get the 5th unit repaired and in six months, I plan on refinancing the whole property into a 30-year fixed mortgage. Between now and then, I expect to pretty much break even, due to the higher loan payment and vacant 5th unit. You see, I can’t completely finish the 5th unit before six months is over because I want to refinance this property as a “residential” property, not a “commercial” property. So, the 5th unit will stay “decommissioned” for the time.

Now comes the fun part – landlording. If you want to learn more about my landlording tips, definitely check out “How to Be a Landlord: Top Ten Tips for Success“.

Anyways, that’s the story! If you stuck through this whole time, I sure hope you take a second and leave me a comment below and let me know what you learned or what I forgot! Ask any question, I’ll do my best to help!

This article was written by Brandon Turner and published on April 9, 2013 on biggerpockets.com. The original article can be found here.

PO BOX 551, Liverpool NY 13088